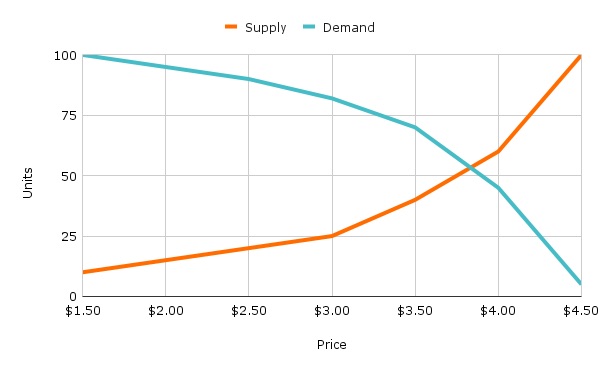

For more than a decade, we've treated parking as a classic market: supply (spaces), demand (vehicles), and price all working in equilibrium. If demand is too high and spaces are hard to find, raise the price. If spots are sitting empty, lower it. It's Econ 101.

You've seen the graph before. As price goes up, demand goes down. Where the supply and demand curves intersect, we get the ideal market rate.

Here's how it typically works in municipal parking:

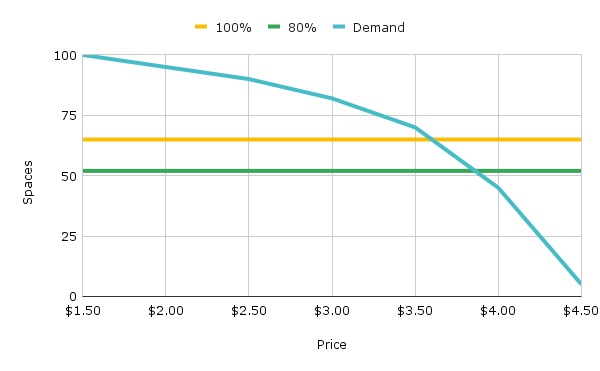

The supply of on-street spaces is effectively static, so we adjust pricing to influence demand. The goal is often to maintain target occupancy — typically somewhere between 70 and 90 percent — so there's a space open on each block.

In theory, this approach makes sense. In practice, it often doesn't work the way we expect.

When price goes up, so does demand

This isn't supposed to happen. But it does.

In the classic Econ market, higher prices reduce demand. That's the logic we've been applying to rate adjustments: tweak the cost to nudge occupancy up or down. But when we look at actual data, we see something different — parking doesn't respond the way the theory says it should.

The following examples use real municipal parking data, pulled directly from Turnstone, before and after rate changes, from 2022 and later.

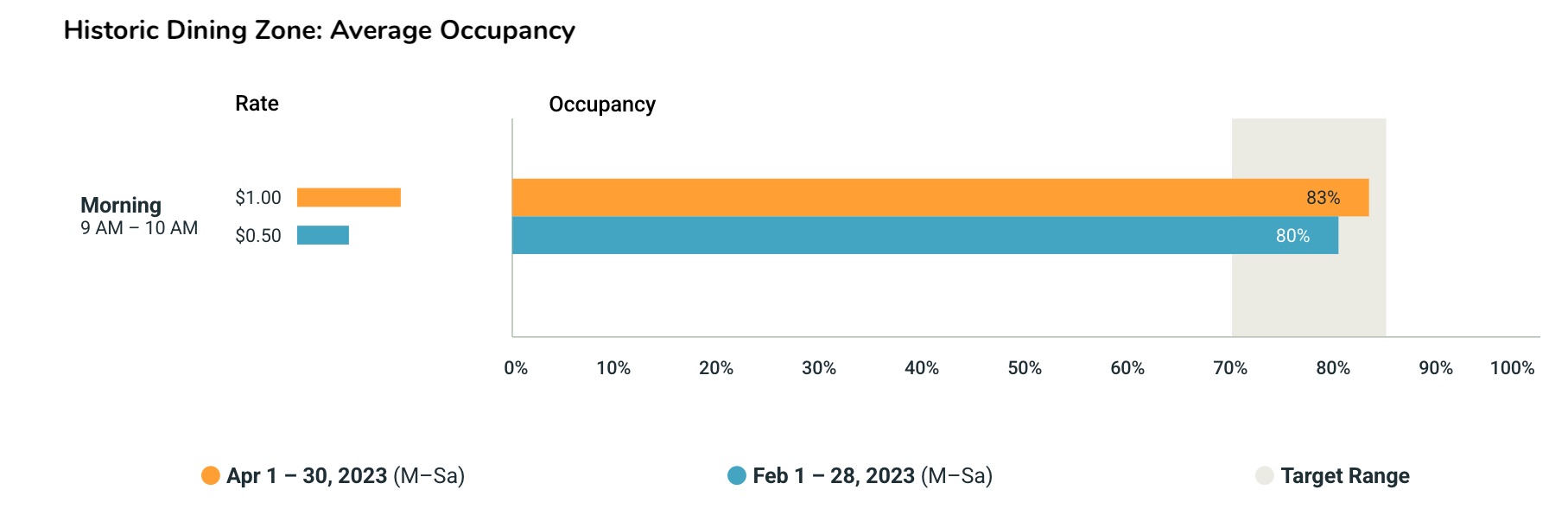

Example 1: Single period rate increase

In this commercial area known for its mix of residential, restaurants, and cafes, the city increased morning parking rates from $0.50 to $1.00 per hour. According to the classic model, this should have slightly reduced demand — especially during a time of day when the area isn't at peak capacity.

Instead, occupancy went up.

Despite the rate doubling in Spring 2023, more people parked. The higher price did nothing to suppress demand.

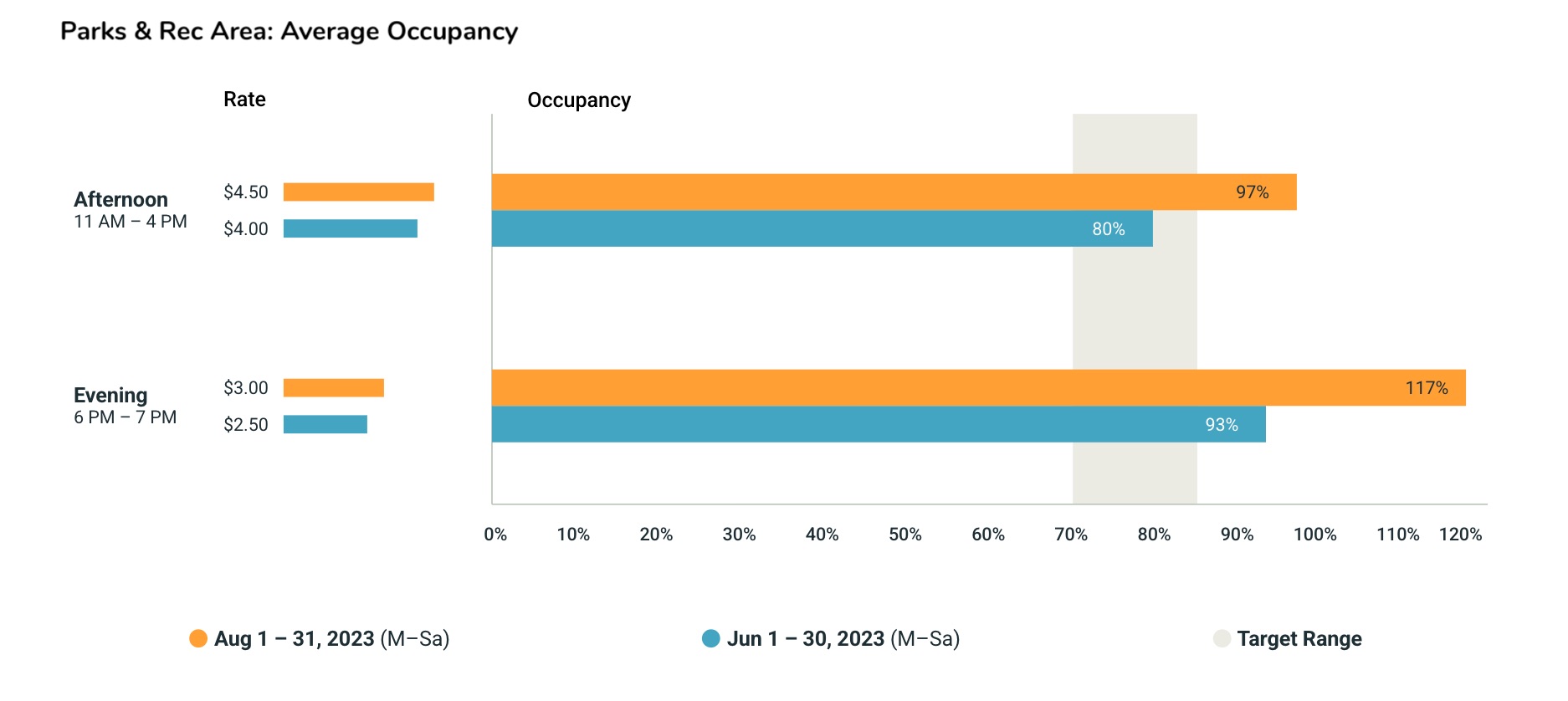

Example 2: Multiple periods in the same zone

In this mixed-use area anchored by public parks, a lake, municipal buildings, and museums, a city raised rates during three different periods: morning, afternoon, and evening. The price increases were modest — $0.50 per hour — but intended to reduce crowding during peak times.

Once again, the theory didn't hold. Occupancy in the afternoon and evening increased following the rate hikes. Higher price, greater use.

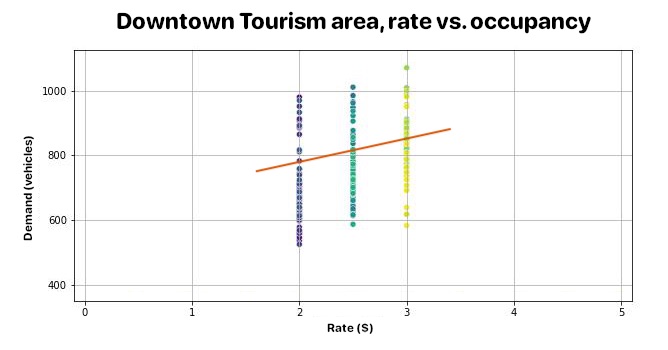

Example 3: Long-term, multiple rate changes

To see if these effects were just anomalies, we took a longer view: three years of data for a busy downtown area. Rates changed multiple times over the period, giving us several price points and a wide range of occupancies to analyze.

When we plotted average occupancy by month against the hourly rate across all Curb Zones and time periods, we found a direct correlation: as prices went up, occupancy also went up.

This wasn't a single anomaly — it was a consistent pattern across dozens of pricing changes (up and down) over multiple years.

These are just three examples, but they point to the same underlying truth: price isn't operating as a predictor for demand. At least not in the way we've assumed.

Why doesn't on-street parking behave like a market?

If higher prices don't reduce occupancy, then we've misunderstood something basic. A few factors might explain why on-street parking doesn't respond to price the way we expect.

Drivers value time and convenience over dollars. When people park, they're not calculating cost — they're avoiding hassle. They want to get from car to destination in the shortest time with minimal friction. A space that's closer, easier to find, or more predictable often beats a cheaper one. Parking may be more like a utility than a discretionary purchase. People aren't shopping around in real time; they're going for the best acceptable option. If a space costs more, so be it — the mental cost of circling is higher than the financial one.

The demand curve assumes price awareness. Drivers rarely have it. Most drivers make the decision to park before they see the rate. For price to influence demand, people need to know what they're paying. In many cities, rate information is unclear, inconsistent, hard to find, or not visible at all until a driver has already committed to a spot. Getting rate details for every blockface to every driver in advance of every trip is virtually impossible.

Elasticity may exist beyond rate caps. We may not be charging enough for price to matter. Even at $5 or $6 per hour, a couple hours of parking can feel cheaper than the total cost — in dollars, time, and inconvenience — of the alternatives. Elasticity may still be present, just at much higher prices that would be unpopular and typically ruled out by policy. We could be setting and resetting prices within a band that's too narrow to get results.

Is it the model or the metric?

The model isn't broken — but our interpretation might be. We've treated price and occupancy as tightly linked, but the data doesn't back that up.

We've seen example after example where higher rates coincide with increased occupancy. We've looked at neighborhoods, time configurations, and even multi-year trends, and the pattern continues to emerge.

The supply-demand model assumes rational, price-sensitive behavior. But parking decisions are often driven by something else: time pressure, convenience, habit, lack of information, or the basic desire to park and move on. Meanwhile, most cities operate with price caps that may be too low to trigger elasticity.

If blockface occupancy isn't obviously dictated by price, does it mean price has no impact? Or is occupancy the wrong metric? Occupancy, after all, isn't a behavior — it's a symptom. People choose to park, and then we get occupancy.

Does price influence other aspects of parking behavior? What about that behavior can we measure instead?

These are the questions we'll attempt to answer in the next post.